Esautomotion (ESAU.MI)

Introduction

Ea is a Italian small cap operating in the automation sector, providing integrated mechatronic CNC systems in the form of software and hardware. The company was established in 2011 as a result of a management buyout from the ESA GV group, which had been active in the industry since 1962 but faced challenges during the financial crisis. The then General Manager, and current CEO, Gianni Senzolo, along with Franco Fontana, who was working as a consultant for companies in the sector at that time, took over the assets of the group and relaunched the business.

Since its relaunch, Esautomotion has delivered outstanding results, pursuing a strategy of internationalization by expanding its operations into China, Brazil, Spain and Portugal.

Industry

Before diving into the business, it is important to understand the industry and explain what is CNC.

CNC is the stands for Computer Numerical Control, a system that uses a computer to control machines that would otherwise require a manual operator. This software guides the machines in aspects such as trajectory, speed and type of operations.

For a visual understanding, you can refer to the following link :

The CNC market is dominated by a select group of manufacturers such as Fanuc, Siemens, or Mitsubishi among others. Determining each company's market share is challenging due to the diversity of machinery and segments within the CNC industry. Fanuc claimed to have a 65% market share in 2020.

Within the market, various niches are occupied by smaller-sized companies. These niches are not attractive to industry giants, and Esautomotion holds a relevant position in several of them.

It should be noted that while the industry has favorable growth prospects, it is also cyclical and can be affected by external factors. An example was the so-called trade war between the U.S. and China that caused a contraction in the industry estimated between 15% and 30%, according to company sources. Fanuc's revenues can be considered a proxy for market behavior as they expect to move at a similar pace to the overall market, recognizing the difficulty of gaining more market share.

With 2018 data the percentage of machines using CNC is in Japan 90 % , Germany 75 % and US 80 %. In contrast, in less developed countries this percentage is much lower. For example, in China it was 29.7% and it is expected to be the country with the highest growth in demand for these machines.

Forecasts from various analyst firms point to sustained growth over the next decade:

- Polaris Market Research: 10 % CAGR between 2023 and 2032.

- Acumen: 8.7% CAGR between 2023 and 2032.

- Fortune Business Insights :7.2 % between 2022 and 2029.

The industry presents high barriers to entry because of the switching costs involved. Specialized training is essential for both operators and engineers since any operational error could lead to costly breakdowns and production stoppages. Moreover, the diversity of machines, even when using similar software, requires specific knowledge and skills.

Business

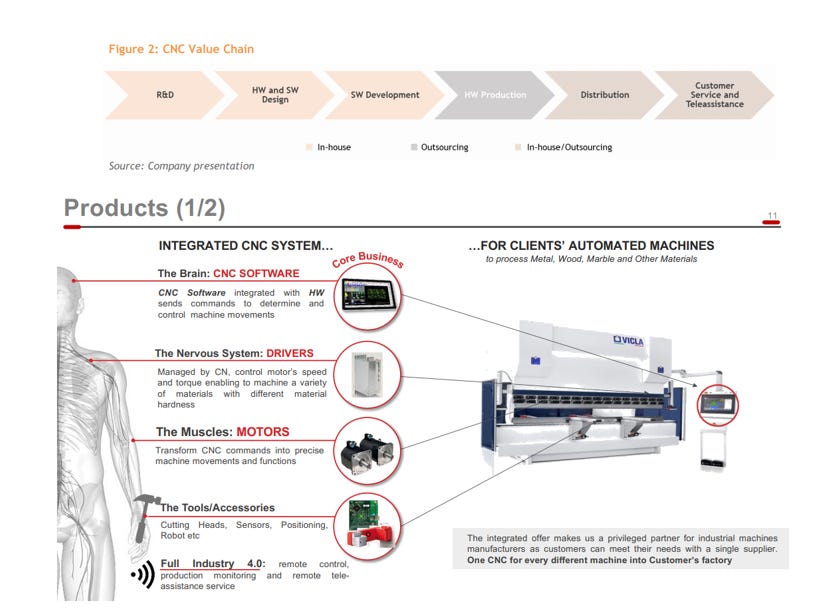

Esautomotion offers high-end products, focusing mainly on CNC software, but also on hardware components, such as drivers, motors, cutting accessories and sensors. The hardware is designed in house but manufactured externally. In addition, after-sales and remote support services are provided.

Esautomotion focus on niche markets allows it to compete effectively against smaller companies, contributing to a strong competitive position. For example, in the woodworking segment the leading manufacturer of woodworking machinery use the company's CNC systems. However, Esautomotion chooses not to enter segments dominated by large companies, such as machine tools. Despite this, the company collaborates with certain customers who request their involvement because companies like Fanuc or Siemens do not offer sufficient customization or technical support.

By offering customized products to these niche markets provides Esautomotion with a significant competitive advantage, resulting in high customer loyalty. The fact that 75% of the company's revenue comes from customers who have been active since 2011 demonstrates the trust and long-term relationships Esautomotion has built with its customers. Furthermore, the consistent revenue growth from these loyal customers at a 13,2 % CAGR from 2011 to 2022.

The following are some examples of the company's customers:

Golden Arrow Water Jet Equipment Manufacturing Co: As a supplier of water jet cutting machines for Tesla's new factory in China, Golden Arrow chose Esautomotion software, motors, and drivers for their machines.

Yawei Wuxi: A leading manufacturer of press brakes in China, Yawei Wuxi opted for Esautomotion CNC solutions for their water jet cutting machines used in BMW's factory in China.

Mitsubishi US: The US subsidiary of Mitsubishi has implemented Esautomotion CNC solutions in their press brake machines. This is noteworthy, considering Mitsubishi itself is a producer of CNC equipment. The fact that Mitsubishi opted for Esautomotion solutions highlights the competitiveness and trustworthiness of Esautomotion products in the industry.

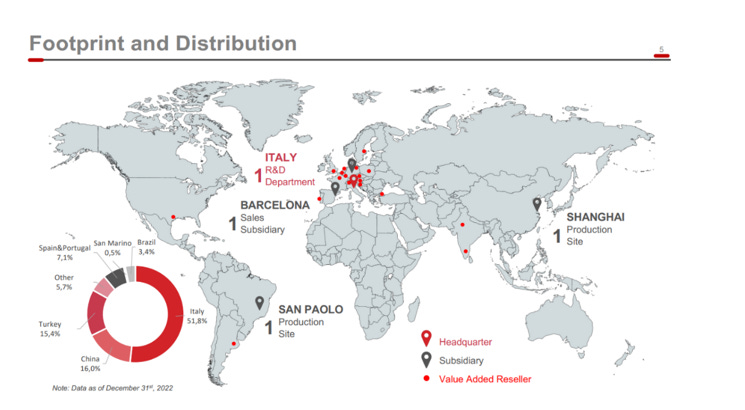

Esautomotion operates internationally, serving more than 360 customers through its 3 subsidiaries located in Brazil, Spain and China and its collaboration with 43 Value Added Ressellers.

The company's growth strategy consists of:

Focus on profitable market niches with synergies with current products.

External growth through acquisitions.

International expansion, especially in emerging markets such as China. Also looking to grow in Northern Europe and the US, with special focus on Germany having hired two senior executives from a leading German company (Power Automation) for this purpose.

To offer lower-end products to access new customers that in the medium to long term will be replaced by medium to high-end products.

In the event of a decrease in demand, the company also adopts a counter-cyclical strategy, which resulted in Esautomotion remaining flat in 2019 and experiencing a 5% decline in revenues in 2020, while the market contracted during these years, and companies like Fanuc saw revenue drops of 12.5% and 20% respectively.

A key strength of Esautomotion is its presence in all segments related to metallic materials.

This is an industry with barriers to entry, so one might ask how the company manages to acquire customers. This is achieved by being present in several segments. When establishing relationships with companies that manufacture different types of machines, Esautomotion tries to offer its products in all segments. This is because OEMs prefer to work with only one type of CNC. For example, consider a company that manufactures bending press machines using Cybelec CNCs, laser cutting machines using Siemens CNCs, and water jet cutting machines using Esauotmotion CNCs. Since Esauotmotion is the only one present in all 3 segments, they will try to get the customer to use their CNC on all types of machines.

Why do customers prefer to use only one type of CNC? This standardizes the products as it is easier for the end customer who will be using the machines to train their operators on one type of CNC, and it also makes it easier to provide technical support.

Capital allocation.

Esautomotion business is an asset light business model, so its main investment is R&D. Part of this R&D expenditure is capitalized, which represents approximately 7% of sales.

Regarding shareholder remuneration, Esautomotion pays a dividend with a payout of 25 %. In addition, the company carries out share buybacks, holding 2.92 % of its capital in treasury shares at the end of 2022. To date, these shares have not been cancelled and the company plans to use them not only for shareholder remuneration, but also to compensate the payment in shares to executives and as a currency for future acquisitions.

The remaining capital has been accumulated and in April 2023 they made their first acquisition since going public.

M&A

On April 22, 2023, Esautomotion completed the acquisition of Sangalli Servomotori, a vertical integration of one of its suppliers that had been providing 12% of the company's cost of goods sold. Esautomotion had maintained a business relationship with Sangalli for over 15 years. Sangalli is a producer and distributor of electric motors, operating since 1957.

The main objectives of this acquisition are to achieve synergies that improve the company's margins and gain access to new customers through cross-selling opportunities. The acquisition was made at a multiple of 6.1 times EV/EBITDA and has a total cost of 10 million euros. Esautomotion acquired a 65% stake in Sangalli with the right to acquire the remaining 35% over the next 4 years.

The payment for the acquisition was structured with a combination of cash and Esautomotion shares. Specifically, 170,000 shares of Esautomotion were granted to the Sangalli family, valued at 6 euros each, which represents a 30% premium over the market price. This premium might indicate that the market undervalues Esautomotion . Massimo Sangalli will continue to lead the acquired company.

Prior to the acquisition, the Sangalli family already held shares in Esautomotion , and currently, they own 4.9% of the company's capital.

Key Executives

Franco Fontana, 63 years old, Chairman of the Board of Directors and one of the founding partners. He holds a master’s degree in business administration and has previous experience in companies such as IBM Italia and Kodak, where he held various leadership roles. From 2001 to 2005, he served as the CEO of CMT Spa, a manufacturer of machine tools, and later worked as a consultant in restructuring Italian and Chinese companies in the machine tools sector.

Gianni Senzolo, 70 years old, CEO, and founding partner. He has a 35-year track record in the CNC industry. Gianni joined ESA GV as the CEO in 2006 before the takeover that led to the creation of Esautomotion . After the acquisition, he retained his position as the CEO of the company.

Andrea Senzolo, 38 years old, General Manager. Before joining the company, he worked as the Sales Director at RedCom Slr, a company dedicated to the manufacturing of laser and plasma cutting machines. In 2012, he joined Esautomotion as the Sales Director, and in 2023, he was appointed as the General Manager. Is the son of current CEO Gianni Senzolo and is likely to be the next CEO of the company.

In summary, the executive team has extensive experience in the sector.

Shareholding structure

Gianni holds 1,000,000 special shares that give him greater voting rights.

Risks

Concentration of customers and suppliers: Due to the nature of the business and its focus on niche segments, Esautomotion faces a high concentration of both customers and suppliers. In 2018, the top 15 suppliers accounted for 80% of the company's components. The company is implementing a supplier diversification policy, and the growth in customer base is gradually reducing this concentration.

Growth through acquisitions: This type of strategy always carries the risk of poor execution, whether in the price paid or in failing to achieve the expected synergies.

Need for continuous innovation: In the fast-paced industrial sector, continuous innovation is essential for Esautomotion to stay competitive and meet evolving customer demands.

Cyclical nature: The cyclical nature of the industrial sector can lead to challenges, as seen in 2011, which triggered the company's acquisition and relaunch by the current owners. Maintaining low debt levels is crucial to withstand economic downturns.

Communication with shareholders: The lack of reports in English may hinder the company's ability to attract international investors. Improving communication channels with shareholders can enhance transparency and investor confidence.

Financials

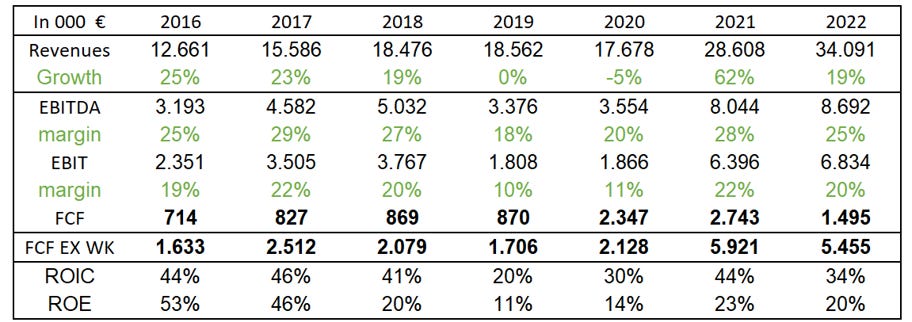

Since its relaunch in 2011, the company has achieved excellent financial performance, with revenue growing at a CAGR of 15.4% between 2012 and 2022. Moreover, the company has generally seen positive margin trends, with occasional dips in 2019, 2020, and 2022. The declines in 2019 and 2020 were attributed to operational leverage and the impact of the trade war and pandemic on revenue. In 2022, the decrease in margins was driven by higher costs of components and raw materials.

Despite its small size and growth, the company has managed to generate positive cash flow, although it has been impacted by an increase in working capital. In 2020, a plan was initiated to reduce working capital levels, but it faced challenges due to supply chain disruptions caused by the Ukraine war. As a result, companies in the industry increased their inventory levels to meet customer demand. However, it is expected for inventory levels and margins to normalize by 2024.

The business's quality is evident through its high return on invested capital, which is supported by the industry's barriers to entry and the company's niche strategy. These factors are expected to be sustainable over time.

Peers

It is difficult to get accurate peers due to the different segments of the industry and/or the specialization of some companies only in software or hardware. For these reasons and the small size of Esautomotion , we will not value it by peers multiple, but I will add two images from the analyst firm KT & PARTNERS to get an idea of the high market expectations and the quality of the businesses, as they are trading at high multiples. It is up to the readers to judge for themselves whether the difference in size justifies such a discount.

Results Q1 2023

The company reports semi-annually, but in a press, release reported that in Q1 2023 it grew revenues by 18.1% and that it continues to encounter difficulties with the supply chain, so it does not appear that margins and working capital will normalize this year.

Valuation

Due to the cyclicality of the business, we will make two scenarios.

Scenario 1

In this scenario we will be optimistic about the industry and use the estimates provided by the analyst firm K&T Partners, which seem quite reasonable. These estimates assume a

normalization of margins and working capital by 2024. In addition, we consider the impact of the acquisition of Sangalli for 5 months in 2023 and full consolidation from 2024 onwards, assuming that the 10 million are paid this year.

Applying a discounted cash flow analysis with a WACC of 10% and a terminal growth rate of 1.5%, we have arrived at a target price of €7.82 per share. Additionally, to obtain another perspective, we will apply a conservative multiple of 10x EV/FCF adjusted to 2026 estimates to obtain a target price of €10.5.

Scenario 2

Under this scenario, we take a more conservative approach, considering the possibility of a temporary downturn in demand due to the cyclical nature of the industrial sector. Based on historical results from Fanuc, we exclude abnormal cases such as the financial crisis and the pandemic, and observe the worst decline in revenues at 14.6%, followed by another decline of 13.9%, with subsequent recovery in the following year. In the event of a market downturn the company has demonstrated flexibility and the ability to withstand the downturn better than the market average, but I find it interesting to take a very negative scenario to get an idea of the margin of safety available.

Applying a discounted cash flow with the same WACC and terminal growth levels as in the previous scenario, we obtain a target price of €3.38. Applying a multiple of 8 times EV/FCF adj in 2026 the target price would be €6.31.

Conclusion

Despite the cyclical nature of the business, Esautomotion is a high-quality company with strong returns on invested capital and significant barriers to entry. The management team has demonstrated alignment with shareholders and a track record of success since taking ownership of the company.

The current price of the stock appears attractive, offering a potential for compelling returns and margin of safety.

In the recent transaction, the company was valued at a 30% premium to its current price, indicating potential upside for investors.

Moreover, the market's expectations for the industry are positive, with estimated growth rates ranging from 7% to 10% annually over the next decade. This suggests that Esautomotion

is well-positioned to capitalize on the growth opportunities in its niche market.

Twitter : @carlosag_92

Disclaimer : The purpose of this article is purely educational and in no way a recommendation for investment.