A few days ago, Verallia reported very good results for the year 2023. We will comment on the most important ones below

Highlights

Revenues of 3,904 million, up 16.5% vs. 2022.

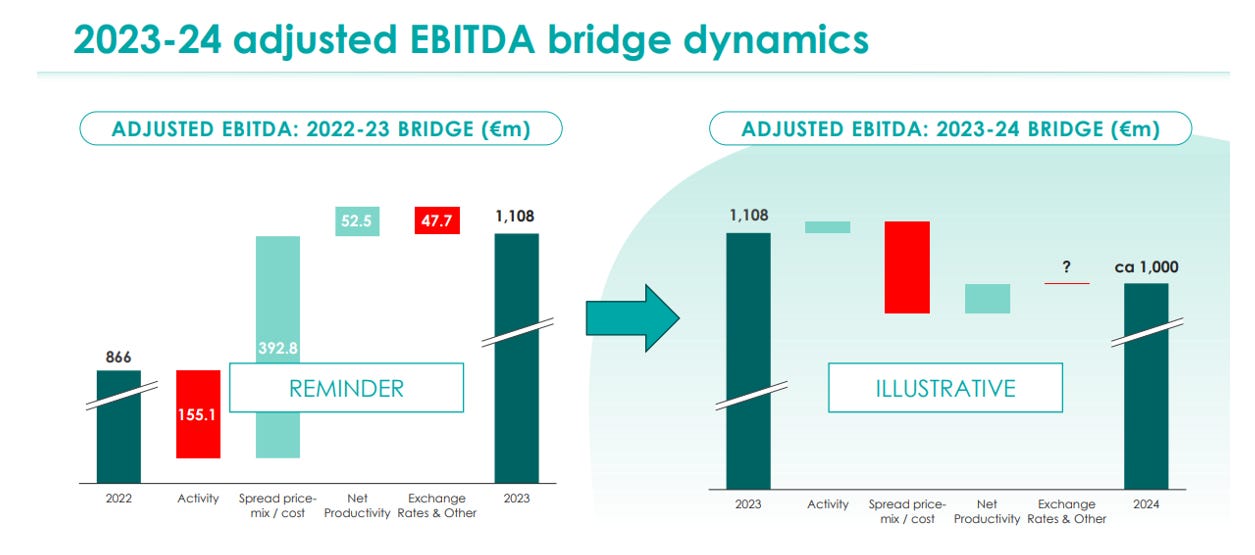

Adjusted EBITDA of 1,108 M, up 28% vs. 2022 with a margin of 28.3%.

Net income of 475 M, up 33.7% vs 2022, and earnings per share of 4.02, up 37.7% vs 2022.

FCF was 381 M despite a working capital impact of 108.2 M. This impact should be 1 time as inventories were at minimum levels.

Management will propose a dividend of €2.15, giving us a yield of 6.2%, with a payout ratio of 53%.

In addition, 42 M has been allocated for share buybacks during the year.

Net debt was reduced by 3%, but due to the increase in adjusted EBITDA, the debt level is 1.2 NET DEBT / ADJ EBITDA vs. 1.6 in 2022.

OUTLOOK

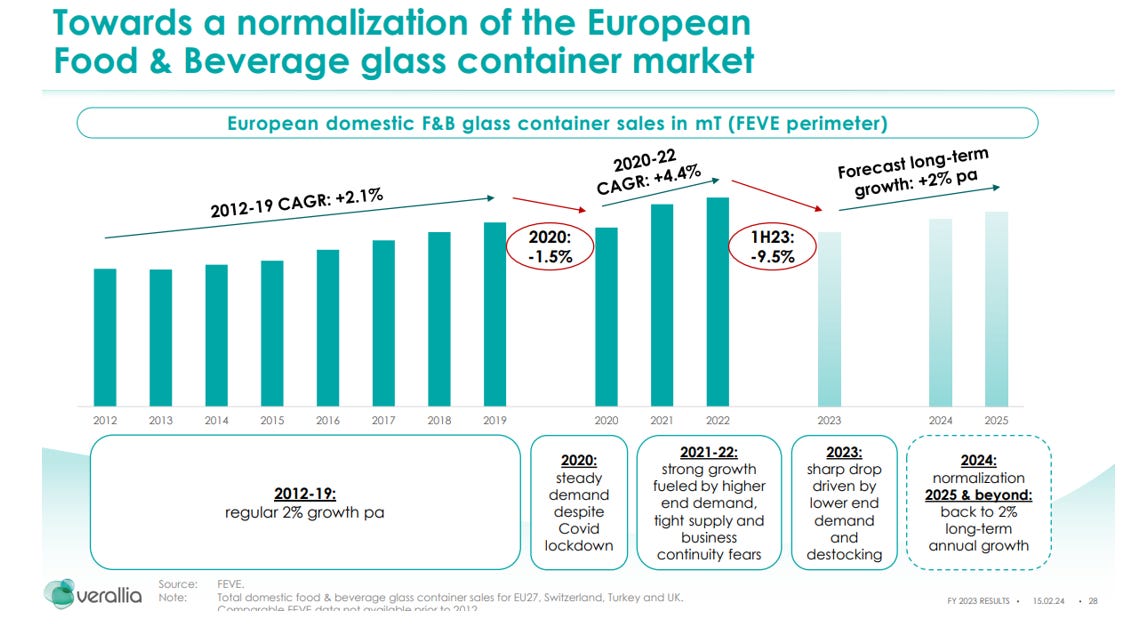

In the years 2020 to 2022, there was an increase in demand. As we have seen in many other industries, due to the pandemic and the threat of disruption to the supply chain, many companies increased their inventories significantly. In 2023, demand for glass containers saw an unprecedented drop in H1 and although there is no official data, the company has said that overall demand continued to fall in H2. This was due to a drop in consumption and destocking by customers. In the conference call, the company reported that customer destocking should end in H1 2024. From 2025, they expect the market to return to a growth trend of 2% per year.

Revenue growth in 2023 was entirely due to price increases. Contracts were revised upward with higher inflation expectations than ultimately materialized. As a result, the 2024 contracts were revised downward.

All these factors have led the company to give an ADJ EBITDA guidance for 2024 of around 1 B, 10% lower than in 2023.

This drop in EBITDA is due to the price cuts. In terms of volume, they expect a negative H1 and a positive H2, resulting in a small volume increase compared to 2023. This will imply a decrease in EBITDA during H1 and an increase during H2 with respect to 2023.

Valuation and Estimates

The company currently trades at 8.1x P/E and a FCF yield of 9.3% and a dividend yield of 6,2 %.

Looking ahead to the next few years, analyst consensus estimates are as follows:

Conclusion

The market is not going through its best moment, but we have to understand that the final demand has not fallen that much, it is just that customers had an excess of inventory and sooner or later this will come to an end. From the second half of the year, the demand of Verallia should be in line with that of the end consumer.

Given the quality and stability of the business, the valuation looks very attractive and management is doing its job well by rewarding shareholders with dividends and buybacks.

Disclaimer: The information contained in this article is for informational purposes only and does not constitute investment advice. The views expressed in this article are solely the author's own and should not be taken as a recommendation to buy or sell any security.