Verallia annual results and valuation

Verallia presented results a few days ago, good results in line with expectations that caused the share price to rise by 7%. I understand that this rise is mainly due to the guidance.

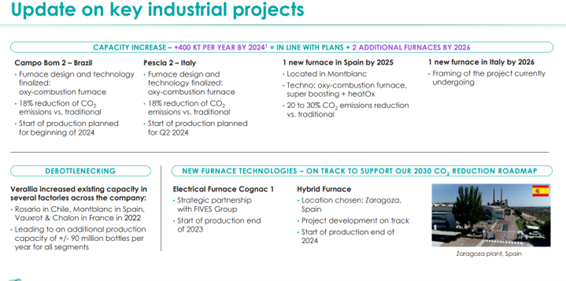

Highlights of the year:

Acquisition of allied glass closed in November for an EV of £315m and revenues of £160m. Allied now Verallia Uk has a strong positioning in premium segments and although they have never stated what margins they have, they said Allied are better that actual margins. Since Allied has better margins than Verallia, the acquisition occurred at a maximum of (applying Verallia's margins) 7.75 EV/EBITDA.

Capex spending has slightly increased from 10% of sales to 11% due to several investments to increase capacity and set up 2 new furnaces by 2026. Maintenance capex stands at 8% of sales with the extra 3% being projects to increase capacity.

Revenue growth was driven mostly by price increases, volume grew by only 1% and they expect the market to grow a little over 2% in the next few years.

The company continues to deleverage a with a current level of Net debt /Ebitda of 1.6 on track to be considered investment grade.

Dividend of 1.4 € per share, an increase of 33 % of this quoted today at 38.02 gives us a yield of 3.7 % in a very stable company that should grow in the coming years at least 10 %.

Guidance

The guidance has been better than expected and they forecast revenue growth of over 20% and continue to improve margins.

In this 20% is included the acquisition of Allied, which as it was acquired in November has not been included in the numbers, the real organic growth would be 14% which is much more than what I expected and the guidance they gave in the last years in which they were looking for a growth of 4 to 6%. If inflation persists they expect to continue to generate a positive spread.

Valuation

Considering the acquisition of Allied the company is trading at approximately 12x earnings as we do not know the exact margins of Allied, is still quite attractive for such a stable company with a lasting competitive advantage.

Based on management's earnings guidance excluding margin improvements to be conservative in 2023 the company should generate EPS of €3.36 trading at 11 times next year's earnings.At 15 times earnings our target price is 50.4 euros a 30% discount.

Keep in mind that these are conservative estimates, there are two aspects that we are not taking into account:

1. While revenues should grow by 20%, profit should grow above for two reasons. The reduction in leverage will result less impact of the financial cost on the profit and secondly we are not taking into account the improvement in margins promised.

2. The other aspect to consider is also that the company will continue to buy back shares, even if it is not a significant amount (the authorized buyback program is 50m) they hold 4.1 % of their own shares with the plan to cancel them.

In the long term the company should continue to compound at rates of 4-6% per annum above inflation. It is also likely that they may find more acquisitions.

Conclusion

While I don't expect this company to be a multibagger and the target price is only 30% above plus a 4% dividend, I consider the possibility of losing money here is very limited, especially in times of inflation in which the company has proven to be able to transfer it to its clients and even create a positive spread.

Here you have the investment thesis.

Twitter @carlosag_92