This publication serves as an update to the original investment analysis on WE.Connect, which was published last year:

https://10baggernewsletter.substack.com/p/weconnect-deep-dive-pdf

WE.Connect in a Nutshell

WE.Connect's core business is the wholesale of IT products.

The company is experiencing significant growth, with a Compound Annual Growth Rate (CAGR) of 18.81% since 2016.

WE.Connect holds a strong net cash position equivalent to 24% of its market capitalization, which is likely to be deployed for future Mergers and Acquisitions (M&A).

The company demonstrates a robust Return on Invested Capital (ROIC) exceeding 20%.

Following several challenging years for the industry, multiple catalysts are anticipated to drive increased demand throughout 2025.

WE.Connect is currently in negotiations for a potentially strategic acquisition.

The company is trading at attractive multiples of 6.7 times Price-to-Earnings (P/E) and 2.9 times Enterprise Value to EBITDA (EV/EBITDA).

Introduction

WE Connect Group was formed through the merger of Groupe Unika and Technline on December 17, 2015. The company was listed on Euronext Paris in 2016 under the ticker symbol ALWEC.

The group specializes in the design, manufacture, assembly, and distribution of computer hardware and electronics, with its primary business being wholesale distribution on behalf of third parties.

Business Lines

Distribution on Behalf of Third Parties: WE Connect Group operates as a wholesaler of IT products, functioning as an intermediary in a three-way relationship between major brand manufacturers and mass retailers.

Accessory Manufacturing: WE Connect Group offers a comprehensive range of consumer electronics products designed, assembled, and distributed under its own brands.

Customized PC Design and Assembly: WE Connect Group possesses its own in-house assembly line, enabling the company to offer a variety of customized PCs to individual customers and institutional clients.

The Company's products are sold to specialized supermarkets, large and medium-sized retailers, computer resellers, and specialized e-commerce platforms such as Fnac, Boulanger, Carrefour, and Leclerc, as well as through online marketplaces like Cdiscount and Rue du Commerce, and the company's own websites, including www.mgf-info.fr and www.pcafrance.fr.

The main products sold include computers, monitors, multimedia products, storage solutions, printers, consumables, and accessories (such as cases, phone accessories, tablets, and connectors). Additionally, the company offers a variety of other electronic products, including electric scooters and electric bicycles.

Major milestones and events over the years

2016: Initial Public Offering (IPO). As part of their international strategy, the company decided to discontinue the distribution of third-party products and focus on their own branded products. Launch of the GAMIUM brand, specializing in gaming accessories

2017: Acquisition of PCA FRANCE and HALTERREGO. Set a sales target of €100 million for 2018.

2018: Strategic agreement with Kuwait for the distribution of the WE brand. New agreement with HP for the distribution of accessories in France. Partnership with the LENOVO brand for the distribution of its IT and peripheral products in France. Commencement of construction of the new headquarters, consolidating all the Group's offices into a single location, alongside a new logistics warehouse with double the capacity of the previous one. Achieved sales of €122 million, exceeding the €100 million target set in 2017. Established a new sales target of €200 million for 2022.

2019: Expansion of the collaboration with ACER, signing a new agreement for the exclusive indirect distribution of PREDATOR and NITRO gaming accessories in France. Extension of the agreement with HP to include the distribution of their entire range of PCs and laptops.

2020: Achieved €211 million in sales, surpassing the 2022 target of €200 million ahead of schedule.

2022: Acquisition of DYADEM and OCTANT, along with its logistics platform SHAM, marking the company's entry into the printer and supplies business, which offers a more recurring revenue stream compared to consumables. Signing of a new national distribution agreement with EPSON. Launch of "WE SECONDE VIE," a new initiative планируется to offer reseller customers, starting in early 2023, a buy-back service for their old IT equipment and smartphones, as well as a new commercial offering of refurbished products. This new activity aims to further enhance customer loyalty.

2023: New agreement with HP to distribute its products for the business and public sectors, including PCs, monitors, workstations, accessories, and services, such as HP ProBook, HP EliteBook, and HP Dragonfly notebooks, as well as ZBook workstations.

2024: Acquisition of MCA TECHNOLOGY, an IT wholesaler specializing in serving professionals.

Business Overview: The Distribution Business

The Company's core business is third-party distribution. This business is characterized by low margins and a light fixed asset base, with working capital representing the company's primary investment.

The company's value proposition for both manufacturers and customers is as follows:

Manufacturers:

Increased reach: Access to a broad customer network, enabling suppliers to reach a wider audience without the need for significant investment in marketing and sales.

Reduced logistics costs: The wholesaler assumes responsibility for inventory management and shipping, lowering logistical expenses for manufacturers.

Mitigation of financial risks: The wholesaler takes on inventory and non-payment risk.

Working capital financing: The wholesaler typically pays suppliers more quickly than large retailers such as Carrefour, providing them with faster access to funds.

Customers:

Outsourced logistics: Warehousing and shipping are managed by the distributor on their behalf.

One-stop shop: Access to products from various brands without the need to establish individual relationships with multiple manufacturers.

Working capital financing: Flexible payment terms and potential credit lines offered by the distributor.

The company distributes products from over 30 technology brands, with whom it has established strong, long-term partnerships over the years. Some of these include:

WE Connect also holds exclusive distribution agreements in France, such as the one with Acer for the exclusive indirect distribution of PREDATOR and NITRO gaming accessories.

Own Brands

Leveraging its logistics infrastructure and established relationships with customers and suppliers, the company complements its third-party brand distribution by offering its own brands. These brands compete in the low-cost segment. The company does not disclose the specific percentage of sales generated by its own brands.

The company's portfolio of own brands includes:

WE: Offers a wide array of accessories for tablets, smartphones, and laptops, including bags, cases, and speakers. It targets a broad audience as well as specific segments such as gamers, children, social network users, and remote workers. Beyond its core product line, the company is agile in capitalizing on emerging market trends for technology-related products, such as self-balancing electric scooters and set-top boxes for televisions. Essentially, if they can replicate a technology product and offer it at a competitive price, they will.

D2DIFFUSION: Specializes in sound, image, and multimedia connectors.

HEDEN: Focuses on video surveillance and home automation solutions.

Halterrego: Specializes in audio products.

Gamium: Dedicated to gaming peripherals and accessories

Customers

The company's customer base is diverse, ranging from specialized supermarkets to large and medium-sized retailers, computer resellers, and e-commerce specialists. These include prominent names such as Fnac, Boulanger, Carrefour, Leclerc, Cdiscount, and Rue du Commerce, as well as sales through its own online platforms, www.mgf-info.fr and www.pcafrance.fr.

In recent years, the company has strategically focused its growth on corporate clients, aiming for higher visibility and recurring revenue streams.

The majority of its sales, representing 94.12%, are generated in France. The remaining exports primarily consist of sales to French overseas departments and territories.

Growth Strategy

The company's growth strategy is pursued through two primary avenues:

Organic Growth: This involves establishing partnerships and signing agreements with new brands to expand its product portfolio and market reach.

Growth through Mergers and Acquisitions (M&A): The company strategically acquires businesses that offer opportunities for synergy. These synergies include expanding the product range, absorbing fixed costs more efficiently, and creating cross-selling opportunities by capitalizing on existing customer relationships.

Industry Overview

Its important to note that the wholesale distribution industry, applicable to most products including computer hardware, trends towards consolidation. The main reason for this is that the primary competitive advantage is typically achieved through economies of scale, due to the following reasons:

Obtaining better purchase prices: Larger distributors can negotiate more favorable terms with manufacturers due to higher volumes.

Reducing costs as a percentage of sales: Increased scale allows for greater efficiency in operations, particularly in warehousing and transportation.

Securing agreements with a larger number of brands: Offering a wider range of products simplifies procurement for customers, making larger distributors more attractive partners.

Estimating the exact market size is complex due to the variety of products involved. However, the distribution segment in France, as measured by the British research company Context (January 2025) through a representative panel of distributors, is estimated to be €8.3 billion. This would imply that WE Connect currently holds a market share of 3.4%. According to the CEO, the company is the 4th largest player in the French market and the only one of French origin, with the top three being American companies, presumably referring to Ingram Micro, TD Synnex, and Arrow Electronics. As these companies do not break down their sales in France, individual market shares are not publicly available. However, the fact that the 4th largest player holds only a 3.4% market share suggests significant potential for further market consolidation.

Demand Drivers of the Industry

The industry show certain drivers and characteristics in terms of demand and cyclicality, the most important of which are:

Seasonality: Demand typically peaks in the last quarter of the year due to Christmas shopping and back-to-school purchases.

PC refresh cycle: The replacement cycle for PCs varies depending on their use (home, professional, or gaming), but the average is between 3 and 5 years.

Technological trends: The introduction of new technologies, such as new processors or graphics cards, drives demand for updated products.

Other trends: Positive trends influencing the industry include the growth of gaming and the increasing prevalence of remote work.

Current Market Situation

Although the company sells a variety of electronic products, PC sales serve as a good proxy for the current market situation.

2020 and 2021: Sales experienced significant growth due to the COVID-19 pandemic, which fueled demand for remote work and online learning, resulting in two years of over 10% growth.

2022 and 2023: With the normalization of the market and a challenging macroeconomic environment, PC sales declined by approximately 15% each year (with slight variations depending on the source). 2023 was the weakest year for PC sales in the last decade.

2024: According to Gartner IT, the PC market experienced a modest recovery of 1.3% year-over-year in 2024.

Q1 2025: Sales increased by 4.8% in the first quarter of 2025 (Source: Gartner, April 14, 2025). The increase in sales was primarily driven by the USA and Japan. In the USA, this was mainly due to inventory build-up in anticipation of potential tariffs rather than an increase in end-customer demand. In Japan, the sales increase was driven by the end of support for Windows 10 and the GIGA education Chromebook replacement program.

There are currently three key drivers expected to contribute to positive PC sales in 2025. This is the primary reason for writing this update.

New Technologies: The launch of PCs with integrated Artificial Intelligence (AI) capabilities in the second half of 2024.

Windows 10 End of Life: Microsoft will cease support for Windows 10 on October 14, 2025, prompting upgrades.

PC Refresh Cycle: In 2025, it will be five years since the significant sales growth during the pandemic, meaning many of those devices are nearing the end of their refresh cycle.

Shareholders and Management

The company is controlled by its founders, brothers Moshey Gorsd (51 years old) and Yossef Gorsd (41 years old), who together hold 76.53% of the company's capital.

Capital Allocation

The cash generated by the company has been invested in further growth, either through investment in working capital or inorganically through acquisitions. The remainder is used to buy back some of the shares issued as a bonus to avoid dilution and to pay a small dividend. The dividend was only eliminated in 2020 because the company received government-guaranteed loans during the COVID-19 pandemic.

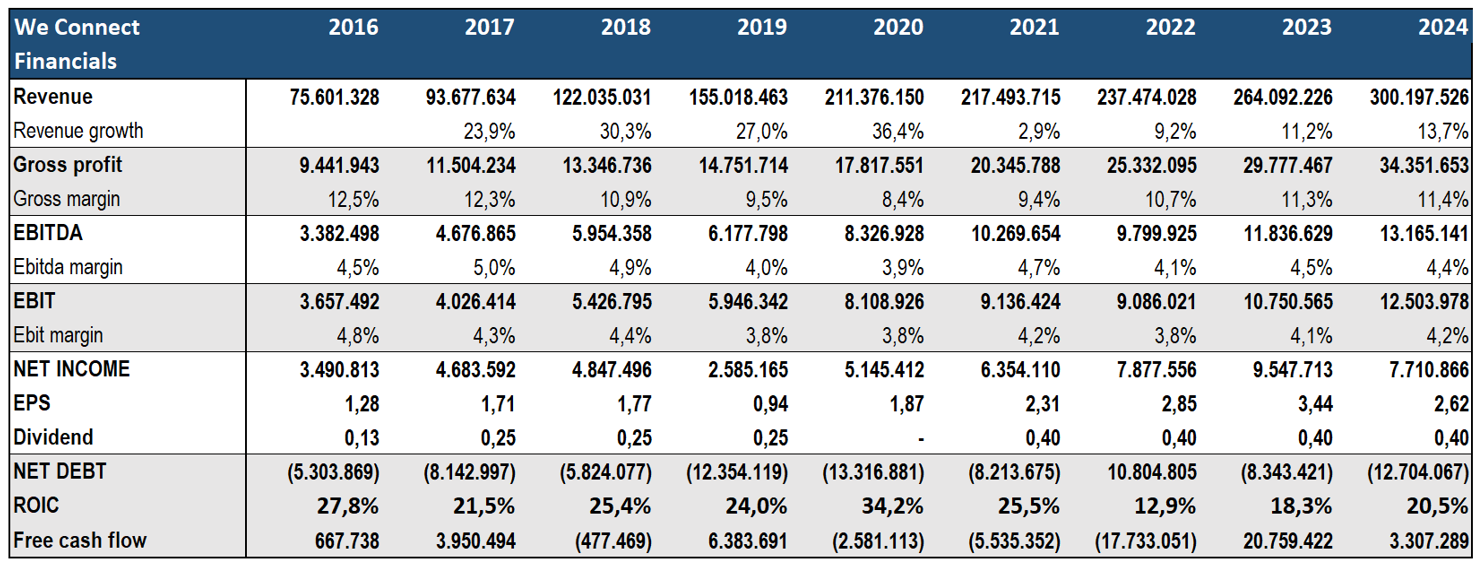

Financials

Revenue: Since its IPO, the company has demonstrated strong revenue growth, accumulating a Compound Annual Growth Rate of 18.81%. This growth has been driven by the consistent reinvestment of its cash flows into both working capital and strategic acquisitions.

Margins: To accurately assess the evolution of profitability, it is more relevant to focus on the gross margin and EBITDA. This is because the company adopts a conservative approach to provisions, and a significant portion of these are often reversed in subsequent periods. As observed in the provided data, following a dip in 2018, the trend in margins has been positive, which can be correlated with the company's increasing scale.

Balance Sheet: The company has historically maintained a very conservative balance sheet, a common characteristic of family-owned businesses. Currently, the net cash position stands at €12.7 million, compared to a market capitalization of €51.6 million.

Return on Invested Capital (ROIC): The company's returns on invested capital have been consistently high, averaging 23.4% since its IPO.

Free Cash Flow (FCF): A common characteristic among distributors is that Free Cash Flow tends to lag Net Income during periods of growth. This is because growth requires investment in working capital. In the company's free cash flow calculation, the cost of acquisitions has been taken into account, as these have been executed at close to book value, primarily consisting of working capital. Given the company's high ROIC, reinvestment is a rational and value-enhancing decision.

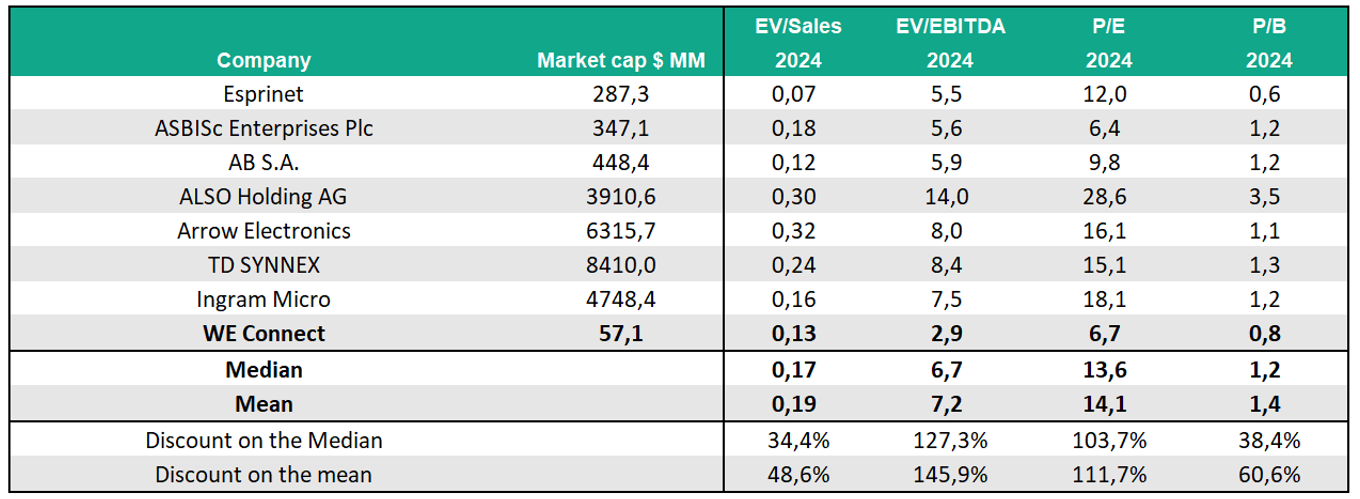

Valuation

1. Comparables:

2. Historical Valuation:

The company shows a significant discount across various valuation metrics, both compared to its peers and to its own historical trading levels. The company's limited market attention appears to be a primary reason for this undervaluation. The lack of coverage is so pronounced that financial data providers like TIKR and Market Screener have yet to update the company's 2024 financial results.

Looking Ahead: A Return to Organic Growth and M&A as Value Drivers

After experiencing a 5.4% decline in organic growth in 2024, the company is expected to resume organic growth this year.

A rebound in organic growth is expected, driven by three catalysts that support an industry recovery: the introduction of AI-powered PCs, the end of Windows 10 support, and the start of the PC refresh cycle for devices sold during the pandemic surge.

Second, MCA Technology was consolidated in the second half of 2024, contributing €50.3 million in revenue. While the exact contribution for the first half is unknown, it is generally understood that the second half is seasonally stronger. This suggests that MCA's contribution in the first half will be slightly lower but still significant. For context, MCA generated €110 million in revenue in 2023.

In the annual report, the CEO indicated expectations of double-digit growth in 2025. Furthermore, a sales target of €400 million for 2025 was announced in mid-2024, coinciding with the acquisition of MCA.

M&A:

In April 2025, the company announced that it had entered into exclusive negotiations to acquire EXERTIS' consumer activity in France. This potential acquisition is significant for several reasons.

Revenue Contribution: Exertis' consumer activity in France generated €176 million in revenue in 2024.

Premium Brand Portfolio: Exertis France has a wide-ranging portfolio of premium brands that WE.Connect does not currently distribute. This portfolio includes Microsoft, Logitech, and TP-Link. Some of these agreements are exclusive, such as Microsoft's Xbox All Access program. They also include partnerships with innovative companies like Starlink and Meta Quest.

Iberian Peninsula Exposure: Approximately 5% of Exertis's sales originate from the Iberian Peninsula. Although this is currently a small percentage, it could lay the fundation for WE.Connect's international expansion. The company would double its TAM with the expansion into the Iberian Peninsula.

Potential Scenarios for 2025

To illustrate the potential financial outcomes for 2025 based on the discussed growth drivers and the potential Exertis acquisition, we present the following two simplified scenarios, assuming constant margins. I repeat, this is a simple way of understanding the potential, not an estimate or projection.

Based on the information presented and assuming constant margins (without this constituting formal estimates), we arrive at the following potential scenarios for 2025:

Scenario 1: No M&A: Based on a market recovery and the company achieving its €400 million sales target.

Scenario 2: With Potential Exertis Acquisition: Assuming the company achieves its €400 million sales target and includes the potential revenue from Exertis (€176 million).

Scenario 1 implies sales of €400 million. Maintaining constant margins would result in a net profit of €10.3 million. Scenario 2 implies sales of €576 million and a net profit of €14.8 million. This would result in a price-to-earnings ratio of approximately 5 in Scenario 1 and 3.5 in Scenario 2.

Conclusion:

Based on current trading multiples, the company appears to be sufficiently undervalued to consider investing in it. Furthermore, considering the anticipated catalysts for 2025, which are expected to drive a return to organic growth, coupled with the potential acquisition, I believe the upside potential is significant.

However, it's important to acknowledge that the company is small and has low liquidity, which is likely a primary factor contributing to its current undervaluation

Disclaimer: Please note that this document does not constitute investment advice, but rather reflects the personal opinion of the author, who currently holds an investment in the company. The author assumes no responsibility for any misuse or misinterpretation of the information contained herein. Readers are strongly advised to conduct their own independent research and consult with a qualified financial advisor before making any investment decisions.

Hello Carlos,

Thanks for your write-up. I noticed in the 2024 Annual Report (Note 6.8, p. 119) that donations were pretty high (€1.47 million in 2024), while reported EBIT was only €12.5 million. In previous years, donations weren't insignificant either.

Do you have any idea which organizations received these donations? Why did they donate so much? Does the company or its shareholders benefit from it in any way? Is there any indication that these donations went to a related party?

Do French companies avoid publishing financial reports in English, or am I just looking in the wrong place?